Quite a few members have recently contacted us with the same problem. Put simply, they are concerned that they are running short of money far too often and that they urgently need a re-set. Some members have chosen to proceed to an advice appointment. Others have just wanted to know the types of options they might have so they can think about them for a while.

There’s no right or wrong way to approach this challenge and every individual in retirement is different, with different circumstances, needs, wants and attitudes towards money. For this reason we are sharing a five-step plan to manage retirement income and ensure you get a good night’s sleep, every night. These steps will allow you to break down what may appear to be a very big problem, into a series of smaller steps so you can consider every aspect of your money management and how to best approach it. The first three steps address some useful ways to maintain a balanced budget; the last two look at the bigger picture of how your savings and investments might be structured.

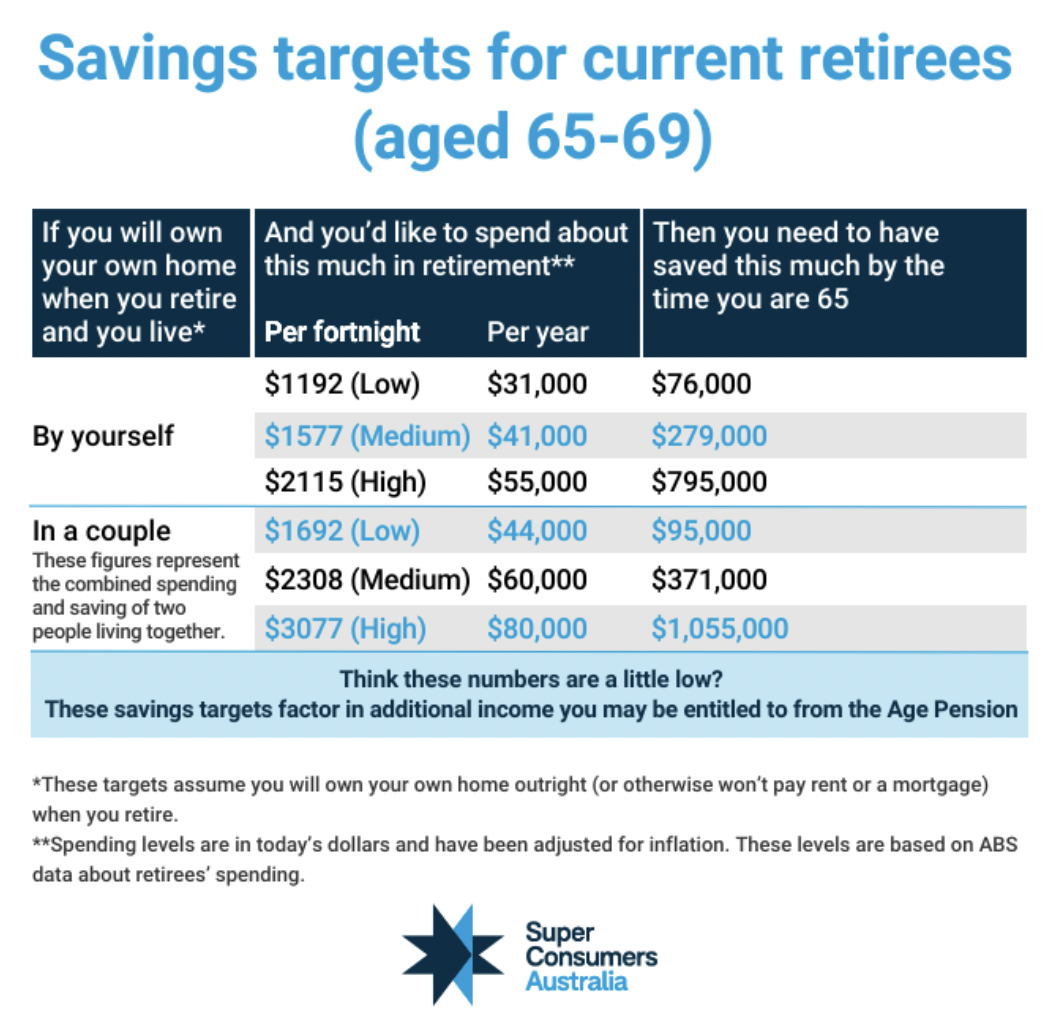

And to get you started, here’s a reminder of some conservative savings (and spending) targets offered by Super Consumers Australia (SCA) which is part of the Choice consumer advocacy group:

Now let’s see how you might achieve your retirement goals, while living within your retirement budget.

Five steps to better money management:

- Know thyself – What’s your household expenditure?

- How do you manage debt?

- Entitlements are there to be used

- What can you access?

- How will you make the necessary changes?

Know thyself – household expenditure

How much does it really take to run your household? The recurring (often rising) costs are often easy to track. But how much are we spending on essentials? And how much on non-essentials? This is important as it helps us identify if we are stressed about our expenditure when we could actually do something about it. Or, are we failing to cover the absolute essentials with no room for discretionary spending? One quick way to measure this is to create a list of your monthly expenditure. Try downloading credit card expenses and merging them with your bank account outgoings in one master spreadsheet.

Next take three highlighter pens. Mark in green the absolute essentials (rent, mortgage payments, food, insurance, energy bills, water etc). Mark in pink the desirable, possibly necessary expenses (e.g. gym membership, garden maintenance, gifts for grandchildren). Last, take a yellow pen and mark the truly discretionary expenses (holidays, flowers, books, movies, wine, chocolates, entertainment expenses). This allows you to see whether you really are living on the brink. Or if some judicious trimming might reduce your spending enough to allow you to live within your means. Another important thing to note is the ratio of pink, green and yellow. In theory yellow (discretionary) will be the category with the lowest number of items. Is it? And green will probably be highest, or perhaps similar to the number marked in pink? There is no right or wrong here. The important thing is to know what you are spending and why. And through this knowledge to reduce expenditure on items you don’t really need (forgotten subscriptions or club memberships or impulse purchases).

How do you manage debt?

Maybe it’s not your expenditure that is getting you down? Maybe it’s the cost of servicing debt – or the stress of juggling it – that is so challenging? Let’s unpack this. As you will be aware, there is what the economists call ‘good’ and ‘bad’ debt. ‘Good’ debt is generally associated with loans used to purchase assets that will appreciate over time – real estate, share investments etc. You borrow to purchase, the asset appreciates, and your costs of borrowing are far outweighed over time by your overall capital gain.

Then there is bad debt, for instance outstanding credit card balances or personal loans used to fund holidays or renovations you couldn’t actually afford. Even though a mortgage on the family home is technically ‘good’ debt, in the current climate of rapid interest rate increases, mortgages can become unmanageable for those on fixed incomes. You can start by looking at the benefits of repaying or maintaining your mortgage in retirement to understand the impacts of debt and your home.

First things first

There are a few ways of managing debt, the first is that the most expensive debt is the one that should be tackled first. So if you are not able to pay off your credit card every month and are therefore paying exorbitant fees on the outstanding amount, you would be smart to look at a balance transfer card (with an interest free period) or accessing some funds from other savings to put a stop to this haemorrhaging. Personal loans are likely to be less ‘expensive’ than credit card debt, but if they are difficult to repay, a visit to your bank to request a repayment pause is a good move. It can be difficult to judge whether your mortgage repayments have become unsustainable. This is a conversation best had with an accountant or financial adviser who is able to assist you to understand the true value of your property, different ways of managing outstanding home loan debt and how this fits with your current income needs.

Entitlements are there to be used

We’ve talked about this before, but it’s truer than ever. Entitlements are there to be had and used. This starts with your Age Pension entitlement. Is it maximised? Have you checked that your assets are correctly entered? That you have not double listed assets as income as well? That household goods and your car are correctly valued. Are you using your Pension Concession Card as much as possible? Do you ask for seniors’ rates on tours, in hotels and at the movies or local club? Two of our members were recently in London and asked for a seniors discount on the ‘Hop-on, Hop-off’ Red Bus – which resulted in a £34 discount – nearly $70 AUD for the day’s ticket. Ask and you will probably receive.

And then, of course, there is the Commonwealth Seniors Health Card. If you are a holder, you are entitled to the current Federal-State Government energy rebate. If you don’t yet have one, you’ll miss out. This card is also a valuable discount card for medical services and pharmaceuticals so make sure you are not paying more than you need to if you have yet to apply.

Can you access extra funding?

Many retirees have wealth which is tied up in their super or their homes. This is not necessarily a first resort for debt reduction, but it is fair to acknowledge that rather than suffer from ongoing financial stress, it’s worth exploring whether using some of your super or your home equity will help you manage better. Some retirees will choose to use a lump sum payment to reduce their mortgage and thus their repayments. Discussing this beforehand is important as it is useful to know all the ramifications before you do this, including losing a line of credit if you fully pay off a loan which has a redraw facility. Accessing home equity is now a more option, as Federal Government legislation now requires that borrowers can never be left with negative equity. There has been a spike in the Federal Government’s own household equity scheme (HEAS) as people decide to fund their longer lifespans by using their household wealth. Other reverse mortgage lenders will offer more capital than the Federal Government, but usually charge higher interest rates.

Which changes can you make?

Only you know how cash-strapped you really are and how this is affecting your equilibrium. We’ve outlined some of the ways of measuring your outgoings, curtailing them, increasing entitlements and discounted services and the two assets you may be able to access for a balancing of the books. But just because you can do something doesn’t mean you have to. This is where it’s helpful to take a pause, review your current budget and think about the solutions that will work best for you. You don’t have to accept the status quo. You can weigh up pros and cons of different courses of action and then decide on the one with the most upside for you and those you care about. Problems halved and often more easily solved, so sharing this exercise with a partner or trusted ‘other’ is a great idea.

Do you need assistance

There is a lot of assistance to be had for those who feel overwhelmed financially. Start with the totally independent Financial Counselling Australia service, including their debt helpline if your need is urgent. Separately, the Australian Bankers Association offers a financial assistance hub for specific types of debt.

Many of the questions and strategies outlined above are covered by Retirement Essentials tailored consultations for people who need bite-sized advice to manage their retirement income and entitlements. Here are some that could suit you when you are ready to undertake a guided review of your retirement income possibilities:

Retirement Forecasting (Compare two scenarios of how your assets and income will look during your retirement journey).

Understanding more about super (Assess the options to help make your super work better for you).

Maximising your entitlements (Assess any changes you might be able to make to maximise your Centrelink entitlements)

Understanding impacts of your home (look at the benefits of repaying or maintaining your mortgage in retirement)

In the illustration example above it sets out that a couple hoping to have a medium amount of income per year of $60k would have to have combined super of $371k.

The combined age pension for a couple is $43k per year which would require a drawdown from super of $17k to meet the $60k target.

However, going on the 8% that my super has accumulated on average over the past 10 years, $371k would generate approximately $22k per year thus not affecting the $371k balance.

Hi William thanks for reaching out. You can read more detail about the underlying assumptions from the Super Consumers Australia directly. It is great that you are invested comfortably and earning on average in excess of the minimum withdrawal limits of a 65 – 74 year old (5%). From the assumptions Super Consumers states on their site, they have assumed a full age pension and the 5% minimum withdrawal amount from the super. In your situation, your super balance is likely to grow over the near future providing you with greater minimum income. This could provide you with additional spending opportunities in the future. If you are interested in exploring what this could look like for you, you could book a Maximising Your Entitlements consultation to compare a couple of scenarios

I have retired in Thailand and as such I am classed as a “non-resident” for tax purposes. Meaning I have to pay 32.5% tax on every dollar I earn, including my age pension. Is there any way I can legally avoid paying tax on the age pension?

Hi Anthony, sorry to hear you are paying such a high rate of tax. We are unable to help provide taxation guidance unfortunately, you may be best to consult with an accountant or tax professional that specialises in a Non-resident tax situation. Best of luck, Nicole.