Staying the course has long been the preferred option for superstar investors like Warren Buffet and Vanguard founder, Jack Bogle. What does this mean? It means taking a long term perspective on your investments. This can be easier said than done during a year like 2023 when international conflicts, rising inflation and central bank uncertainty led to increasing volatility in money markets across the globe.

But those who held their nerve and did take a longer term perspective are being rewarded when it comes to super fund returns. This is reflected in the most recent update from SuperRatings which summarises Australian super fund returns across calendar year 2023. No matter which way you view these results, it underlines the fact that superannuation remains a solid investment which has performed well across the years. Here’s a quick summary of SuperRatings update.

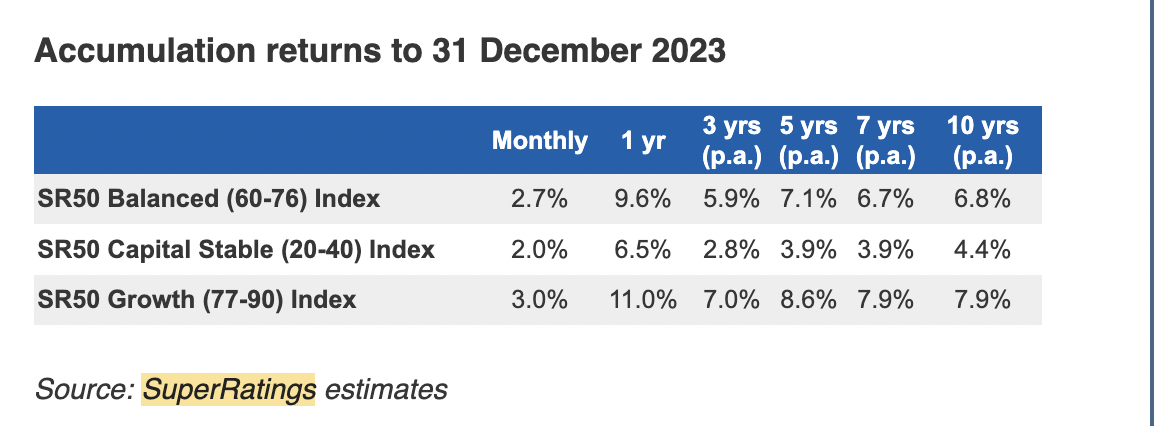

Overall performance

A quick explanation of the table

Balanced options have 60 -76% of their investment in what are known as growth assets such as domestic and international equities (or shares) and property. The rest is in defensive assets such as cash and fixed interest. The capital stable options in this table have only 20-40% in growth assets while the growth options have 77-90% in growth assets.

The median balanced option showed a 9.6% return for the full 2023 calendar year. This comes after a 4.8% loss for calendar year 2022, so it’s quite a remarkable turnaround.

What about growth and capital stable options ?

As shown in the above table, the median growth option returned 11% across the year. The median capital stable option was well behind at 6.5%.

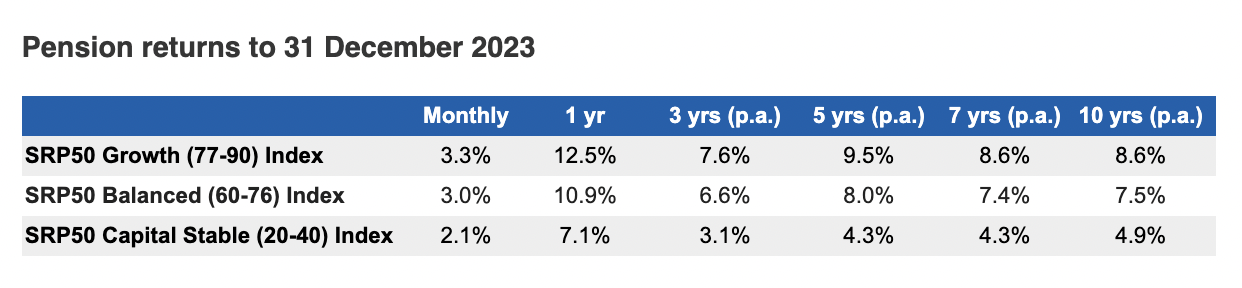

How did pension funds perform?

Even more strongly than accumulation funds! The returns for the balanced pension funds (those which are in decumulation mode) 10.9% for the calendar year and 7.5% over the past 10 years.

Why are returns so strong?

Says Joshua Lowen, Insights Manager, SuperRatings,

‘International shares are the standout performer over the year, with strong growth in technology shares a major factor. These returns were also supported by Australian shares as well as rising cash rates and improving fixed interest and cash returns.

2023 has been a strong year for funds, and rising cash rates will be a relief for retirees needing to access their super; however, inflation remains higher than cash returns and balances are likely to bounce around over the coming year. Even in retirement, superannuation needs to last for the long term, and staying focused on your strategy is key to maximising your chances of success.’

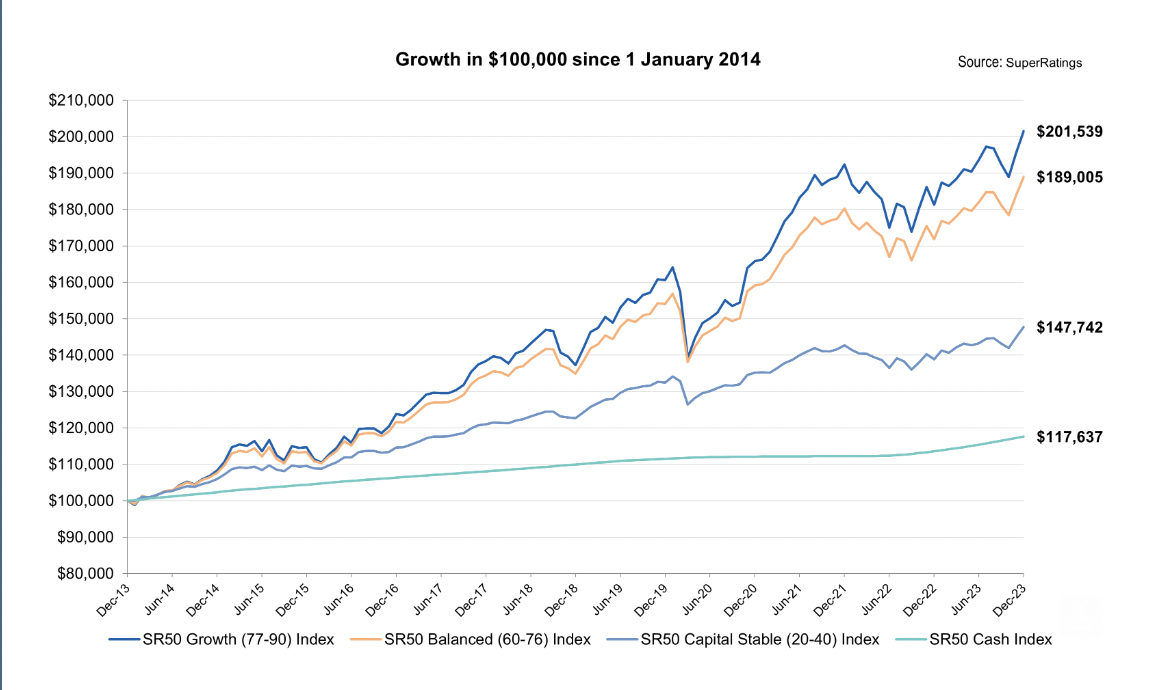

How do returns in super compare to those in cash?

The following chart says it all, really.

This shows an investment of $100,000 in a median balanced option fund over ten years now being worth $189,005. If invested in a median growth option fund it would be worth $201,539. The same amount invested in cash would be worth %117,637.

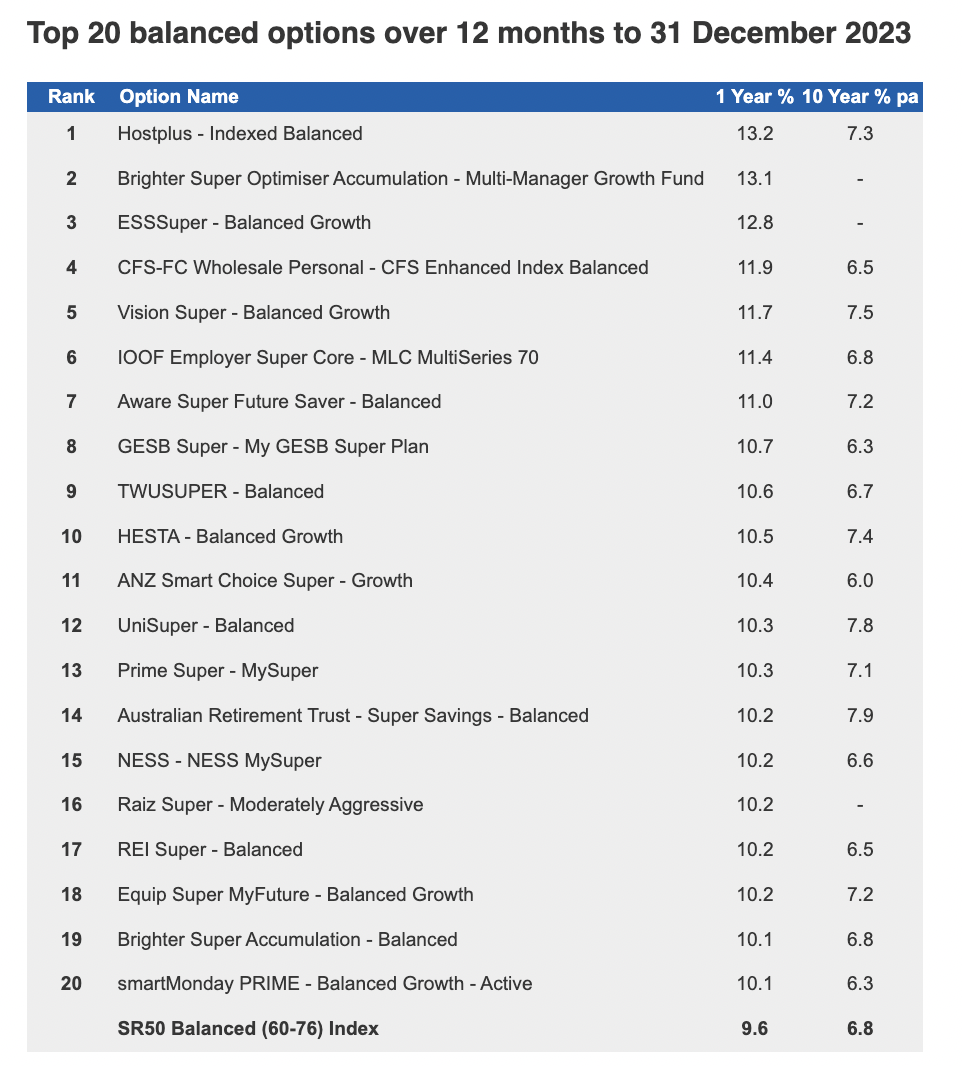

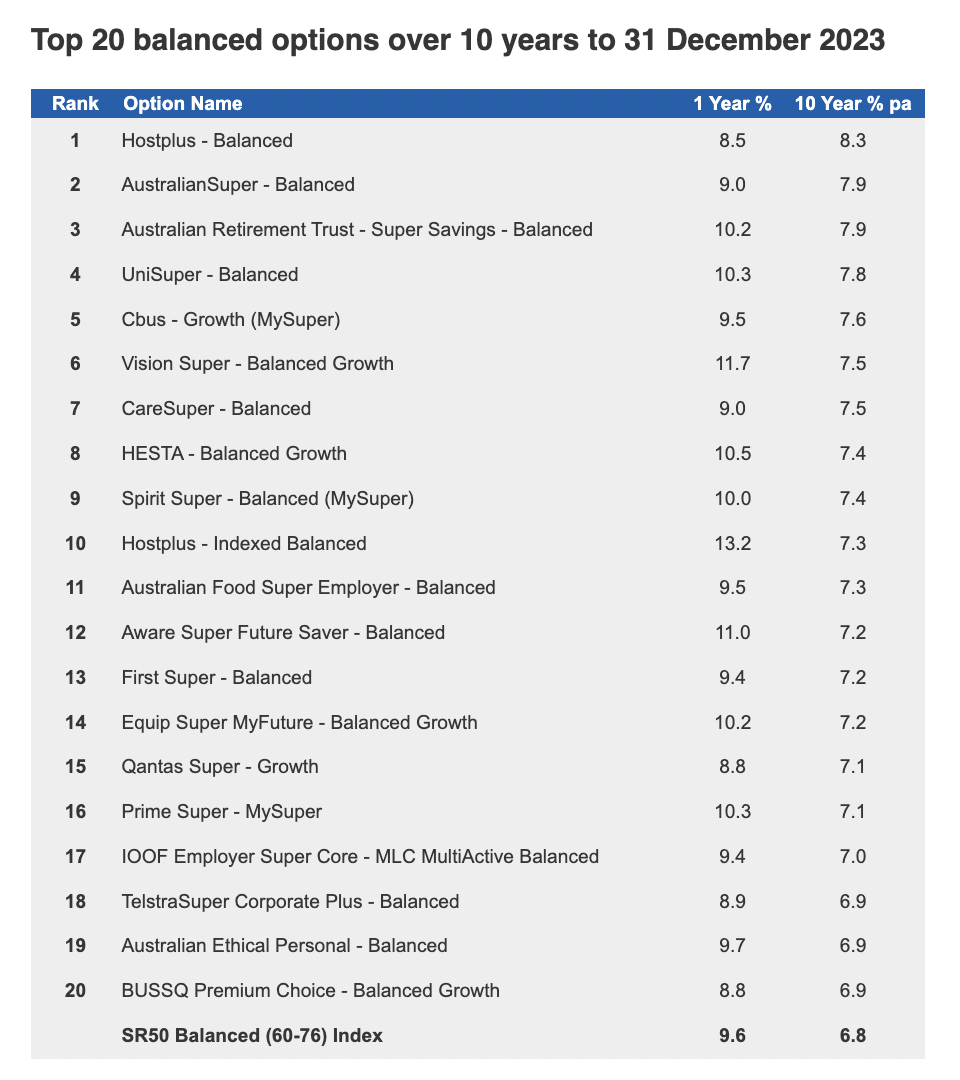

Which funds performed the best?

The following table lists the top 20 balanced options funds for 2023.

What about longer term fund performance?

And here are the top 20 funds over the 10 years to 31 December 2023

How do these returns affect you?

Frequently reviewing your investment settings is a smart strategy. Many retirees can automatically default to conservative settings, without actively thinking about it, even though they may have 20 or more years expected lifespan in retirement. At the risk of stating the obvious, even a small change in such settings can translate to higher income. If we look at the chart showing returns on $100,000 over ten years, the return on growth against balanced was $22,000+ higher. A handy bonus for retirees who could do with some extra discretionary spending power.

If you feel you might benefit from reviewing your own super investment settings, it could help to talk to a Retirement Essentials adviser and do some scenario comparisons using the Retirement Forecaster tool.

How did your fund perform last year? If it’s not listed above, you may wish to check the calendar year returns directly with your fund and then compare these results with the median performances above.

What’s your view?

Are you, too, a fan of ‘staying the course’?

Or is this easier said than done once you hit retirement?

We’d love to hear your thoughts.

This article is provided by Retirement Essentials Representative Number: 001260855. We are an authorised representative of SuperEd Pty Ltd ABN 88 118 480 907 AFSL #468859. This information is not intended as financial product advice, legal advice or taxation advice. It does not take into account your personal situation, goals or needs and you should assess your own financial situation, consider if the information is suitable for you and ensure you read the relevant Product Disclosure Statement (PDS) if you choose to make any changes to your financial situation. It is always advisable to consult a financial adviser before making financial decisions.

Brighter Super Balanced pension fund, went backwards 22-23 and current financial year 24 has not made much either.

So the Australian Super penalty payout has obviously slammed our return for the year. Not making the top 20 is enough to start considering alternate fund

My thoughts exactly. It’s no good them saying that their performance over 10 years is better because this year’s result will reduce the 10 year performance.

I have been tracking my own super fund for the past 7 years, recording values every 6 months. I have a pre-populated chart that shows contributions plus varying interest options for multiple scenarios and I can tell you my fund (one of the one’s on your chart) has only returned 4% over that period, way below their stated goal of CPI plus 3.5% or the impression given above of around 8%.

I wonder why there is this discrepancy? It makes a lot of difference if the performance is really 4% instead of 8%.

Thank you for your informative report. I partly retired a few years ago working as a CRT , only work a couple of days a fortnight, I will be receiving my pension in September. And was comforted to see my Super fund on the list of best performing. I will now take your advice and get some further assistance with my super. Looking forward to future emails from you.

I have now been retired for 10 years and I’m with Equip balanced fund scale….

I pay myself 5% per annum and find with other income from shares that we can manage quite well…

I have not needed to take a lump sum out so the returns minus fees and monthly payments have meant I have more in the account now than when I started…..

I feel that this has been a good long-term outcome…

My super is with HUB24. Investment advisor yesterday stated that my return for the year after fees was 10.78%

Not ready yet to start to draw down as I have guaranteed work of 7.5 hours per week for the rest of the year.

I never see results for them advertised anywhere, why?

I’d agree with Ken & Neil, I’m also monitoring my Super and the returns over the last 2 years have been dismal. My estimate is I’m about 15% behind my long term projections. It’s very disappointing to see that AustralianSuper didn’t crack the top 20 but is 2nd on 10yr chart. The way I see it, we have no choice other than to stay for the long haul.

You have every choice. You can move your nestegg to where ever you want.

Your comments about Australian Super are pertinent though. I have been an Aussie super member since 2018 and I must say, I am disappointed with their performance.

Aussie super were supposed to be the flagship of Industry Super schemes. Hah! Not so!

For further insight, read the various review sites (eg, product review etc) to get an idea of Aussie’s reputation. I decided, after an issue I had that they couldn’t resolve, to give them one more year to lift their game.

Evidently that hasn’t happened.

Flagship funds like their naval namesakes need work to slow down their course to becoming outdated. The bigger the fund the harder it becomes to keep up above market average performance. The longer the fund is in existence the more members move to pension phase the more liquidity they need to keep, the more liquid the asset the lower the returns. Except when interest rates are rising and liquidity kept in Cash. The main reason pension funds returns are up is the increase in cash rates

what do people think of HUB24? Does anyone have experience with them?

I’ve been with REST super for about 15 years. I draw the minimum pension and still hold some money in the super box as well. They seem to have fallen off the best performing list in recent years. Do you have any thoughts about this fund’s long term petformance?

My thoughts exactly. It’s no good them saying that their performance over 10 years is better because this year’s result will reduce the 10 year performance.

Im looking to switch super funds due to dismal returns over past couple of years but am more conservative balanced type investment strategy person ( retired with an account based pension plus part Govt Pension) – currently with Active Super so any recommendations appreciated

Thanks

Scott Pape, the Barefoot Investor guy, recommends Hostplus Indexed Balanced fund, based on returns and investments, also on fees.

I moved there on his advice 5 years ago.

I see this year they are top fund.

Over 10 years they are no 13 fund; AND Hostplus Balanced is the top fund.

They’re worth a look.

I’ve been with AustralianSuper for many years and have been disappointed by their performance and their non action throughout the years when the returns were in the negative.

Because I don’t contribute to my Super account, I can clearly see the ups and downs in the account and its only now, in 2024, that I am back up to the amount I was many years ago, (not sure how long that will last) so when people say long term, long haul, it still doesn’t make keeping all my money in Super easy to do. Its too volatile for me, I really don’t think Super is as good as it should be, so I keep the majority of my money in the bank, where I am always assured of a positive return.

Thanks so much to everyone who has shared their thoughts and experience of recent fund performances. As you will be aware, it’s not appropriate for Retirement Essentials to make comments about any individual funds. We can, however, remind readers that past performance is a poor indicator of future performance. It is difficult to make comparisons of super funds, even for professionals. There are many things to consider (fees, asset allocation, management approach, etc). Maybe we need to share an article on Comparing Super Funds and why it’s so difficult? Would this be helpful?

Yes please

Yes please, as it would make informative reading.

My super is with Hostplus which appears to perform well across the short, medium and long term.

I finished work in July 23, however my wife enjoys her work and will continue to work for the time being.

I therefore haven’t converted my super to pension phase as we don’t require any additional funds until my wife finishes work.

However my understanding is that this means my super in accumulative phase is subject to costs that I would not be subjected to if I switched to pension phase.

Is my understanding on these super costs/fees correct, and should I switch over into pension phase and begin withdrawing the mandated 5% since I am 70 years old ?

Hi Greg. Thanks for your comment. You are correct that if you move your super into a pension product you will be required to draw out the minimum amount. In your case 5%. You are not forced to spnd it however. You could reinvest it elsewhere. The big advantage of having super in the pesnsion phase is that the earnings are untaxed. In accumulation the earnings are taxed at 15%. It is this tax on earnings that is the additional costand it can make a big difference. the best way to determine whetehr you might be beter off moving your money from accumulation to an account based pension would be to book an appointment with one of our advisers. I have added a link to our superannuation consultations.

Hi Kaye,

I am in the process of amalgamating two super funds and would welcome a competing superfunds article and sooner rather than later please!

Trade union influence in many a concern

And on the retail-fund side: the corporate greed, profiteering for shareholders, and charging fees for no service (including deceased account holders) in many are concerns.

I am about to inherit $100k. I’m single, working 4 days a week, turning 60 in April. I don’t own property. Am I better to put my inheritance into my balanced Hostplus fund, or my bank at 5.5% interest?

I am considering a temporary retirement this year, to access lump sum to purchase a retirement village unit.

Hi Helen, good on you for planning ahead for your retirement rather then waiting until it is upon you! You do have a few options to consider so it is worth understanding the pros/cons and long term impacts of each. The best way we could help you with this is via a consultation which you can book HERE.

My Super is with REST have never seen them in you reports.