Keeping Retirement Simple – Part 3

In the last Keeping Retirement Simple article, we discussed how your retirement horizon impacted the amount you can afford to spend. The longer you need to plan for, the less you can afford to spend each year.

This time, we deal with the second major uncertainty in retirement: how much you’ll earn on your super and savings/investments.

Retirement Principle #3: The more you earn on your investments, the longer your savings will last and the more you can spend.

Sounds pretty obvious…but it might surprise you to know the difference it can make.

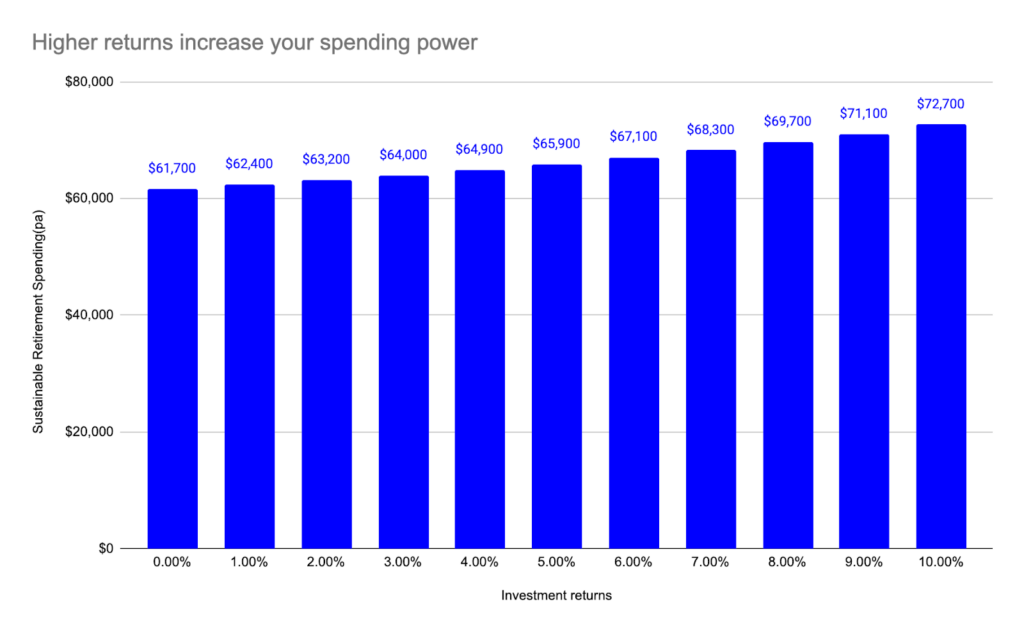

Here’s a way to see the impact. This chart shows the sustainable spending rate for various levels of investment return for a 67 year old couple with $500,000 in super and savings, planning on a retirement horizon till age 92. If they put their money under the mattress and earn nothing, they might be able to spend $61,700 per year (made up of Age Pension entitlements + savings). However if they were to earn 7% per year through a sensibly invested super fund, they might expect to spend $68,300 per year.

Of course, we don’t know what investment returns we’ll get in the future on most investments. And returns can be volatile (lots of ups and downs). Generally, too, higher returning investments entail more short term volatility.

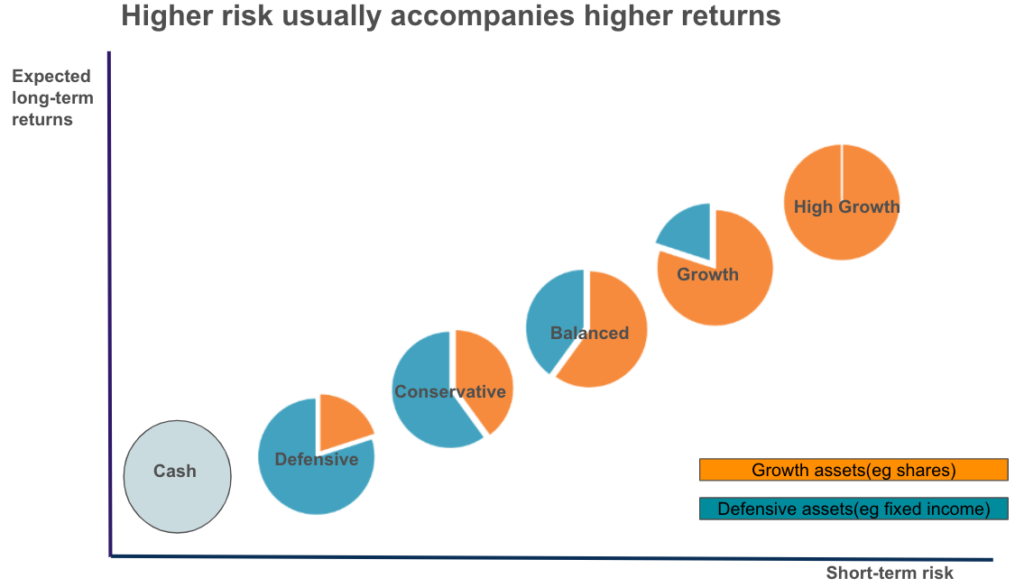

Think of shares of Australian and international companies. They’ve offered the highest returns over time…but come with the disadvantage of greater volatility – more risk of short term loss.

Super funds and investment firms usually offer a range of investments from cash to all shares, as shown in this chart. The diversified portfolios in between cash and all-shares each hold a different mix of asset types to see diversification of risk and reduced volatility. They are labelled as Conservative to High Growth indicating the dependence on more conservative fixed income type investments or growth assets such as shares and property.

The super fund returns for the past decade are shown in the table below showing the most popular categories.

| Annualised returns | Cash | Conservative | Balanced | Growth | High Growth | All Shares |

| 10 years to December 2023 | 1.5% | 4.4% | 5.6% | 7.0% | 8.1% | 9.0% |

This was a good period for investment in growth assets…and a not so good period for cash. Since 2023, cash rates have picked up a little. Going forward, it’s likely that the high starting levels of the share market will mean that returns of riskier assets will be moderated compared to their recent history.

Most investors will want a diversified portfolio and not just cash (returns too meagre) and not all shares (too risky). The level of growth depends on how you weigh off risk against return. If you can’t tolerate the risk, there’s no point in going for the higher return. It’s really important to “stay the course” if you’re going with riskier investments – not back out when things get tough. It can help to understand your personal risk tolerance. Our advisers can help you to work that out.

For those retirees who are on the Age Pension, there’s good news in that you effectively have an inflation protected fixed income portfolio providing steady growing income. If you’re a part Age Pensioner you may also get an increase in your Age Pension if your assets drop due to a market downturn as happened in the Covid market drop of 2020. In this way, the Age Pension acts to buffer the falls of your riskier investments.

What’s the upshot? The investment choices you make in your retirement will have a key bearing on your sustainable level of spending. While we don’t know what future returns will be, we can plan for a range of outcomes and make some intelligent decisions to help deliver an attractive retirement income.

Case Study:

Martha and John were approaching retirement. They had about $750k in super and investments between them. Their super had done well, earning a return amounting to about 8% per annum over the past 10 years. But, facing retirement, how were they going to invest the money. Would they take it out of the fund and put it in the bank? Or add to their non super investments? Or leave it in the super fund’s account based pension to earn tax free income as they drew it down to fund their retirement spending.

Martha and John booked a Retirement Forecasting appointment which helped them see the implications of their possible investment choices. They realised that putting it all in bank deposits would leave a lot of potential return on the table and reduce their likely retirement income. Better to continue to seek a higher return through a mix of growth and fixed income investments. Their super fund could provide an option suitable to their risk tolerance. Converting to the Account Based Pension meant that their earnings and withdrawals would be tax free.

There are a lot of complex issues at play when retired and considering how to invest. In addition to trying to boost your retirement income you have to consider your personal risk tolerance and also the possible implications on your Age Pension entitlements. The following consultations with our advisers can help you to work through these issues.

- Retirement Forecasting (look at what your income, assets and spending could look like over your retirement).

- Understanding more about super (get the most out of your super in retirement).

- Maximising your entitlements (making the most of your financial resources and Centrelink)

Coming up in our next article: A key principle of retirement planning is matching your spending with what you can afford. Principle #4. Match your spending with what you can afford.

This article is provided by Retirement Essentials Representative Number: 001260855. We are an authorised representative of SuperEd Pty Ltd ABN 88 118 480 907 AFSL #468859. This information is not intended as financial product advice, legal advice or taxation advice. It does not take into account your personal situation, goals or needs and you should assess your own financial situation, consider if the information is suitable for you and ensure you read the relevant Product Disclosure Statement (PDS) if you choose to make any changes to your financial situation. It is always advisable to consult a financial adviser before making financial decisions.

Hi there

I don’t understand Jeremy’s comment that a couple with $500,000 in super/savings could put it under the mattress and still get 61k pa for 25 years. The cash would run out in approximately 9 years, ie when they had just turned 76. Well short of age 92!

Hi Ian, thanks for keeping us honest! I’ve updated the wording to try and avoid confusion moving forward but the $61,700 is not made up solely of the customer’s super/savings, it includes their Age Pension entitlement also. For example if they were eligible for the full couples’ Age Pension then it would be $43,752 of Age Pension plus $17,948 of their super/savings. This is why their personal money would last until their 90s because the majority of what they are spending is Age Pension.

Intrigued by the math. You state by doing nothing with your $500,000 “under the mattress” it might last till age 92. Can you explain how this would work? As above statement…

“This chart shows the sustainable spending rate for various levels of investment return for a 67 year old couple with $500,000 in super and savings, planning on a retirement horizon till age 92. If they put their money under the mattress and earn nothing, they might be able to spend $61,700 per year.”

Even with a full pension I can’t see how you could possibly afford to spend $61,700 annually until you are 92. Further details on this calculation would be appreciated.

Hi Susan, thanks for keeping us honest! I’ve updated the wording to try and avoid confusion moving forward but the $61,700 is not made up solely of super/savings, it includes the Age Pension entitlement also. For example, if eligible for the full couples’ Age Pension then it would be $43,752 of Age Pension plus $17,948 of their super/savings. This is why their personal money would last until their 90s because the majority of what they are spending is Age Pension.

Cheers Steven, glad I wasn’t the only one trying to make sense of the figures.

How does the granny flat arrangement work in terms of investment, family cohesion and optimizing centrelink payment? I mean selling one’s principal home and using the proceeds of sale as a contribution to the granny flat arrangement with one of the children. Can you lead a discussion on this?

Hi Theodore, great question! The granny flat arrangement can be quite complex with rules applying regarding the reasonableness test. Centrelink payments can be affected depending on the value of the granny flat interest, so a discussion tailored to what you have in mind is recommended. We can help you with these discussions in our Strategy Consultations. I would be happy to help you with this if you would like to make a booking here

The other take home I gain from this is that super (industry super anyway) generally pays better than the bank