The last day of October is the final date when individuals can file their tax returns unless they are represented by a tax agent. Many retirees – those on a Full Age Pension or those whose sole source of income is from their super – won’t be required to file a return. But for the many others who receive income in addition to the Age Pension or super, some tax may need to be paid.

With this year’s deadlines passed, many retirees will have received their tax returns and now be able to review this very useful summary of their finances.

This is a really helpful thing to do.

Firstly, because it puts you in immediate touch with how much money you have earned, and how much tax you have paid. Which then allows you to think and plan ahead for financial year 2023-2024 and make adjustments if you’re paying tax unnecessarily.

Three ways your retirement savings are taxed

Although tax rules can seem very complex, particularly when you get into the finer detail of ‘grandfathering’ and concessional superannuation contributions etc, there are three broad ways your retirement savings will be taxed. Here’s a quick overview.

But first a spoiler alert!

The following overview is just that – a top level explainer of the three different levels of tax for those with retirement savings. They are not offered as advice, but information which will help you understand your own ‘buckets’ of savings. Tax is not the only consideration that matters, so this article may be a timely prompt for you to seek further advice from a financial professional, perhaps your accountant or an adviser, who can guide you in the best way to suit your own particular circumstances. Another important cautionary note is that the Transition to Retirement strategies have some different rules which are not covered below. Again it is important to seek specific guidance on such strategies when considering tax implications.

Retirement savings- Accumulation accounts

These are superannuation accounts in savings mode. They are usually pertinent to those yet to retire, or those who have retired, but have not converted their super savings into an income stream. Generally speaking,Australians under age 60, will have their super in an accumulation account. Age 60 is iswhen you could have the opportunity to access your super. This is also called Preservation Age. Some retirees will choose not to withdraw, instead to keep their savings in accumulation for years after they have reduced hours or left full-time work. This is worth considering, as those who have accumulation accounts will pay 15% tax on earnings in their accounts.

Account Based Pensions

Not to be confused with the government payment of the Age Pension, superannuation pension accounts are those which have been ‘rolled over’ into Account-Based Pensions from which regular income streams are paid. Lump sums may also be accessed from such accounts. Because these super funds are now in ‘decumulation’ mode (i.e. the spending phase of retirement) there is no income tax paid on such funds. The difference between the 15% paid when saving super and the 0% tax paid when withdrawing is significant. And so it is worth considering whether you are paying too much tax if your fund is still in the accumulation phase. We covered this topic recently with an example of how Anne and Michael were able to save $5760 by moving their super. It’s well worthwhile being aware of the tax distinction between saving and spending phases of super.

Money held outside super

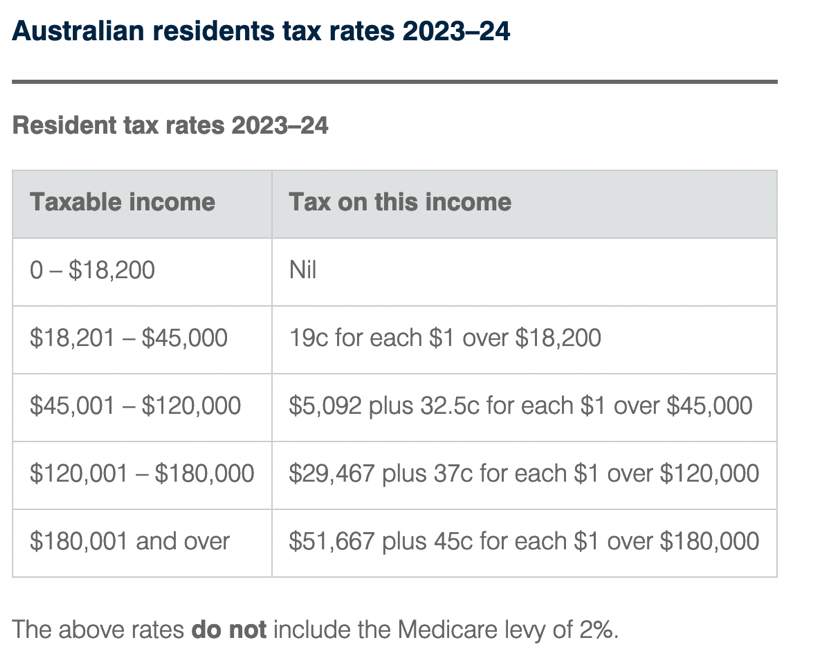

This category essentially refers to private savings and investments as well as monies withdrawn from super and placed in different investment accounts, perhaps cash accounts. It’s not unusual for retirees to consider money in super as ‘locked up’ and money in cash as more available. In reality, your super savings (provided you meet the conditions of release) are as readily available as cash deposits, give or take a day or two. But perceptions can be powerful. This is one of the reasons that some retirees will choose to move lump sums into bank accounts as soon as they are able. But alongside other earnings outside super – rent, dividends, employment income, to name a few – this income will be taxed at your marginal tax rate. Such rates vary, but here are the current tax rates for Australian residents.

Tax obviously depends entirely upon your overall earnings – if you earn less that $18,200 then you pay 0% and progressively more for higher incomes. The main point to consider is, if you are paying tax at a marginal rate which is higher than 15%, then is there another way of organising your retirement savings that can reduce this tax impost?

As we noted above, this comparison of tax rates on retirement savings is designed to give you some extra knowledge to help you to raise the right questions about your own situation, with the right advice professional.

And tax return time is entirely the right time to do so.

If you would like to further explore the tax implications on your own retirement savings, an Understanding more about super consultation will assist you to assess the options available to maximise your super earnings.

What about you?

Do you find discussions about tax difficult?

Do you feel there might be a simple way to tax retirement savings?

Hello,I am in receipt of the full age pension.

occasionally, I am able to do casual work and earn a minimum wage,sometimes not pay ing any tax on the earnings.

To date,I haven’t drawn on my Superannuation but paid tax on my earnings including my pension earned.

Would I be better to invest all my super in a high interest investment account,like a term deposit account?

I am single and get conflicting advice.

What do you recommend or who should I talk to for advice please,sincerely Christine

Hi Christine, thanks for reaching out. There is no single solution that is right for everyone as there are a number of things to consider when deciding on what is best for your retirement savings. I recommend booking a Strategy Consultation by clicking here. We can work through each of the choices you have, and help you determine which options may work out best over the long term. We can factor in considerations such as entitlements, tax and super rules. Best wishes, Nicole.

a brief calculation example for retirees is agood example like what the ato puts out giving a sample calculation of single married with or without partner etc would seem a guide to people calculating or submiting their own tax return and for future years seeing that the interest rate and tax concessions are changging incl the pensioner offests

Hi,I enjoy reading your emails.Would like to see more articles about top level assest limits and how to manage.I am above the limits and would like to know how to manage my long term suitation.

Hi Christopher, thanks for your feedback. If you receive our newsletters we always update our community on changes to upper asset thresholds when applicable. In addition, if you want to have a discussion about what your options may be to reduce assessable assets to help you get below the threshold, or take a look at how far away you may be from eligibility, you can book a one-on-one consultation with one of the team to discuss your scenario in more detail. I would suggest a Strategy Consultation where we can work through a few options together. You can book by clicking here. Best of luck, Nicole

I am yet working, and I have 2 super accounts. One is a pension account from which I receive a pension and the other is an accumulation account into which my employer credits my super. In addition, we also have some bank accounts (term deposits and savings accounts).

When I stop working, both my super accounts will become pension-based accounts.

This is my question: For tax purposes will the income from the super pension and the interest from the bank accounts be considered OR will the income from the super-pension account exempted?

Also, for Medicare levy, will both the pension and the bank interest be considered?

I will be grateful for your response. Thank you.

Hi David, thanks for reaching out. We cannot provide specific tax guidance, but I can provide a bit of factual information. Interest from bank accounts will contribute to your assessable income for tax purposes, as will the majority of any age pension payments if you receive any, but in most cases income from super pensions is not assessable if you are over the age of 60. There are always some exceptions, in particular if your superannuation has an ‘untaxed’ element. This is not common but should be detailed in your super statements. For some help figuring out whether this may apply to you, you can book a General Consultation with us to discuss in more detail, or contact your super fund to enquire.

The Medicare levy generally applies to taxable income only, but I would encourage you to seek further guidance on your individual situation from a tax professional. Best wishes, Nicole.

My only earning is the full pension. Am I liable to pay tax?

Hi Jayv, thanks for your question. This is something that many people have been confused about in the past. The majority of your age pension payment is taxable. However, the government has tax offsets that apply to pensioners that generally mean if you have no other assessable income (or not much assessable income above the pension) you won’t pay any tax as you are below the threshold. More information about this offset is available on the ATO website. You are best to discuss your own personal situation with an accountant or other tax specialist to confirm. Best wishes, Nicole.

I have i small amount of money invested a round figure maybe $10,000 interest a year , would I have to do a tax return and is that added to the pension to give an annual income of approximately $35,000 that I would be taxed on or would the $10,000 interest be considered non taxable as it is under the $18,200

Hi Neville, thanks for your question. We cannot provide detailed tax information but I can confirm that the majority of your age pension payment is assessable for tax purposes, and so any interest you earn would likely go on top of this amount and go toward the calculation of your assessable income for a financial year. Whether or not you need to pay tax depends on the total taxable income. As a result of Senior Australian and Pensioner Tax Offset (SAPTO) your tax liability may be reduced or nil even if your taxable income is a little over $18,200. It’s best to discuss your specific circumstances with an accountant to determine whether you need to lodge a tax return or not. Best wishes, Nicole.

Neville, I believe that you can earn up to $33,000 P/Y when you claim the SAPTO and LITO (low-income tax offset) in tax return without paying tax or M/Care. You can claim SAPTO if you are above pension age.

After 33k tax and Medicare kick in also accountant fees. That extra 2k you have (35,000)

may cost you $700 M/Care,apprx. $200 for accountant plus any tax you have to pay. If you can forgo that extra 2K. if you can, it may save you a few problems and having to deal with a tax agent and the tax department..This info is on the ATO website.Check this if you want but i believe it is correct.

Hello

I am on a full aged pension.

I draw on my super only for an annual holiday or for major vehicle repairs. This may be $2000 or $5000. Does this add as income. Should I do a draw down account and take this money regularly into a savings account rather than draw in big lots from my normal super.

Thanks

Hi Julie, thanks for reaching out! Drawdowns from your super are NOT counted as income. As such, and because you are already on the full pension, you should set up/drawdown your super however best suits you personally. Do not worry about Centrelink as your super is not impacting your Age Pension.